What if “retirement” is outliving your savings? Learn how to adapt if you end up working into your 80s or beyond.

The New Normal: Life expectancy is soaring, and so is the share of seniors still on the job. In 2024, the number of Americans 65+ hit almost 60 million, up 457% since 1948. BLS data show nearly 1 in 5 seniors (19.5%) remained in the labor force in 2024. Yet plans to retire at 65 are fading. As one researcher grimly observed, the idea of stopping work at 65 is “somewhat outdated” – most retirees live 30+ years past that age.

Life’s game has changed: 65 is just the new 50. The U.S. health and retirement study notes the average 65-year-old man now lives to 82½, women to 85+, and plenty push toward age 100. Every extra decade requires more money – and more paychecks. Indeed, economists now tout “working longer” as a strategy to stretch financial resources.

By the end of this guide, you’ll know why the “work forever” scenario is on the rise, how to plan around it, and which pitfalls to avoid. You’ll get step-by-step roadmaps, real-life case studies (meet Sarah and Tom below), checklists, and FAQs on living a 100-year worklife without burning out. Let’s dig deep – your future self will thank you.

Why We are Working Longer

(and What That Means for You)

A generation ago, most men left the workforce by 65. By 1950 about 70% of men 55+ still worked; by the mid-1990s that had plunged to 40%. But since 1995, that trend reversed: older men and women started re-entering the workforce in force. Today’s projections show labor force participation for 65+ doubling: from 12% in 1990 to 24% by 2020, and beyond 27% by 2050. In plain terms, many Americans will choose or need to work into their 70s, 80s or even 90s.

What’s driving this seismic shift? Multiple forces: Longevity, money, and social factors.

- Living Longer, Spending Longer: Simply put, people live much longer, and savings must stretch accordingly. As Bank of America’s financial gerontologist Cynthia Hutchins warns, we need to be “prepared for 100-year lives”. That means 30+ years of expenses after 65. Take Social Security: at 62 you lose up to 30% of your monthly benefit, but if you delay claiming until 70 you get about 8% more each year. In other words, working a few extra years can significantly boost your monthly income down the road – and let your nest egg grow instead of shrink.

- Insufficient Savings: Retirement savings rates have historically lagged. Many never had pensions; 401(k) balances are woeful for low/mid earners. Some estimates say the typical American won’t have even $500 saved by 65 (see Business Insider piece at [57]). People fear running out of money. In fact, 7-in-10 workers (and over half of retirees) worry inflation will erode their spending power. Continuing to earn provides a vital buffer against market swings, healthcare crises and rising costs.

- Health & Purpose: Counterintuitively, working can improve health. AARP cites studies where post-retirement work helps cognitive function and overall health. And there’s mental purpose: many boomers who “quit” their career still crave engagement. They’d rather “keep lunch dates” and use their skills than fade into TV marathons.

- Changing Expectations: The notion of a fixed retirement age is loosening. Pew Research notes that only 29% of current retirees worked for pay, but a whopping 75% of those approaching retirement expect to keep working even after retiring. Employers too are more open: part-time roles, consulting gigs and even “encore careers” are mainstream now.

Modern reality: Many seniors happily at work – or by necessity.

The data and stories agree: Work forever is becoming real. The concept of “retirement” as a permanent 20-year vacation may be outdated. Experts now routinely advise planning to work longer, at least part-time, as a hedge. With that landscape, it pays to face the facts: you may well spend your golden years earning paychecks.

Case Study: Meet Sarah – a Teacher Facing the 100-Year-Old Plan

Sarah from Ohio, age 55, teaches middle school. She assumed she’d retire at 65 with a modest pension and 401(k). But with longevity and costs, her picture changed.

Sarah has saved $300k and contributes to a 401(k), but she fears it won’t last. Her husband had health issues, and they still have a mortgage. She used our worksheet to project costs: living until 90 means possibly 25 years of retirement needs. If she retired at 65 with no more paychecks, she’d need about $1.2M nest egg (factoring inflation) to support modest living, Social Security included. That’s beyond her reach.

Instead, Sarah plans to delay full retirement to 70. Why 70? It’s the sweet spot: each year she delays, Social Security jumps 8%. By waiting, her Social Security jumps by 40% compared to claiming at 66. Plus, she will draw down savings later.

Smart tweak: She also switches to part-time roles after 65. Teaching is physically light, so Sarah arranges a job-share (two teachers split one full-time slot) and supplements it with tutoring online. This eases her workload while still earning.

By 70, Sarah’s plan now looks feasible: savings plus Social Security coverage. Her story illustrates a framework:

- Assess Your Numbers: Sarah calculated her expected monthly expenses in retirement and how much income Social Security will provide at different ages. We recommend you do the same: see if working a bit longer bridges your gap.

- Delay, Even if Gradually: Sarah isn’t stopping suddenly. Transitioning to part-time at 65 and full retirement at 70 spreads the change. This strategy not only increases benefits but also keeps her professionally engaged.

- Invest In Yourself: Knowing that job skills matter at 60+, Sarah took summer courses in online teaching technology. Stay marketable: older workers can command flexible or consulting gigs if they show up-to-date skills.

- Plan B Ready: Sarah also secured a side income – she monetizes a hobby by selling educational crafts online. Diversifying income ensures she isn’t solely dependent on the school’s job.

By age 70, if all goes well, Sarah’s debt is gone and her retirement fund can finally start to be drawn down. The key was not panicking about “work forever,” but making it work for her.

Case Study: Meet Tom – The Choice to Keep Going

Tom from Arizona, 62, is a semi-retired software developer who chooses to keep working.

Tom saved aggressively in his 30s and 40s. He hit FIRE (Financial Independence) by 50 and thought he’d quit entirely. But life threw a curveball: he found the transition to full retirement dull and his spouse expects to live well into the 90s (running in her family). Also, his kids aren’t hitting their college fund. So Tom decided to keep coding part-time.

He advises: If you love your work, let it serve you. Tom’s decision to “work forever” isn’t about necessity – it’s enjoyment and security. He now picks consulting gigs that interest him. Money-wise, every dollar he earns is 100% savings (no more mortgage or kids’ tuition). It dramatically changes his math.

- Lowering Withdrawal Rates: By earning $30k/year, Tom can withdraw a much smaller percentage of his investments. If he’d retired at 55, a standard 4% rule might have overspent his portfolio. With income, he effectively applies a 2% withdrawal to his nest egg, massively reducing burn rate.

- Mental & Social Perks: Tom gets a neuro boost from solving problems; he also mentors young colleagues, staying socially engaged. It keeps him sharp, confirming AARP findings that “continuing to work has benefits for cognition”.

- Tax Efficiency: Now over 62, Tom is smart about income: he maximizes retirement account contributions each year and intentionally stays under limits so as not to trigger higher Medicare premiums. He even delays Social Security to 70 (getting that 8% bump each year) while this income flows.

Tom’s path shows a positive scenario: Working forever by choice can enhance your retirement, not just postpone it. Whether out of love or strategy, those extra years on the job can give you flexibility – and a higher life quality – as long as you plan smartly.

A Step-by-Step Framework to Plan Your (Long) Career

Whether it’s necessity like Sarah or choice like Tom, the approach is similar. If you might work into old age, here’s a blueprint:

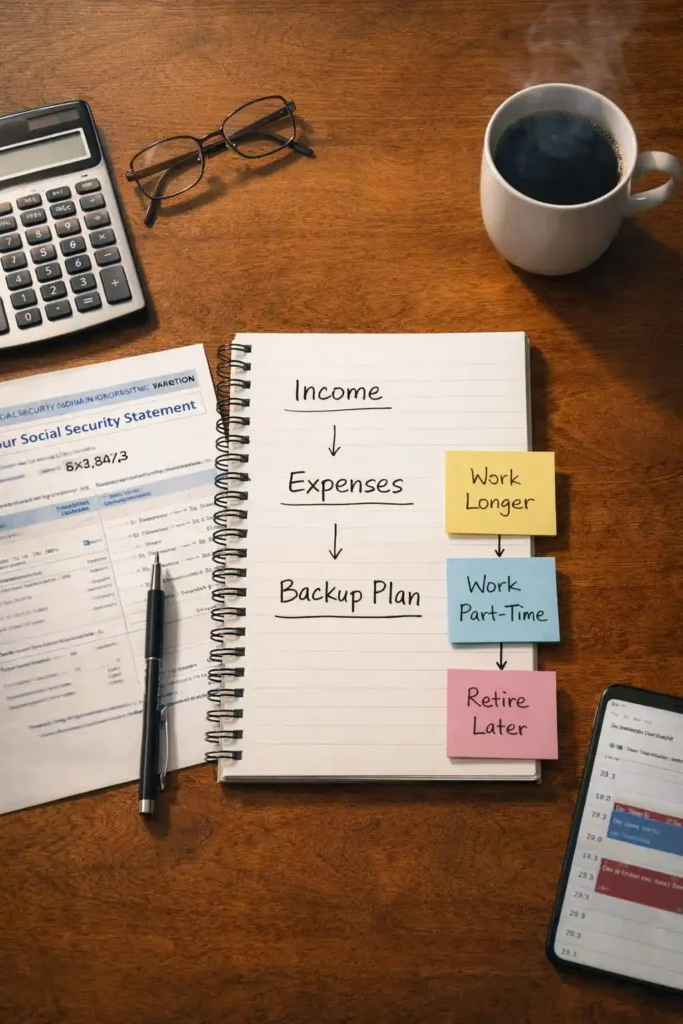

- Frame Your Time Horizon: Realistically estimate how long you might live and work. Use tables or lifespans from research – e.g. 65 today could be 85-90. This might mean 20+ years of work. Project your retirement spending needs for that entire period (even if you retire late, you still need a cushion).

- Crunch the Numbers Now: Calculate current savings vs. target. Tools like retirement calculators can show gaps. Factor in Social Security at different claim ages. If you plan to “work forever,” simulate scenarios: what if you only rely on paychecks and minimal savings? (Dangerous.) What if you delay retirement 5 years? Often, working a few extra years is the single most powerful way to meet your goals. A Boston College researcher sums it up: “Working longer is a really powerful lever to increase the money available in retirement, because you’re not drawing down your savings”.

- Optimize Social Security: Make every year count. Each year beyond full retirement age boosts your benefit by 8%. Conversely, claiming early can cost you a third of your benefit. If working longer is on table, delay taking SS.

- Invest Extra Earnings Wisely: Any income you earn past 65 can go directly to filling gaps. Put it in a taxable account or even better, keep maxing retirement accounts if available (some 403(b)s, IRAs allow 70+ contributions). This buys future flexibility.

- Protect Against Risks: Have an emergency fund and consider disability insurance. At 65+, losing income due to health or layoffs is a disaster. Build a buffer now so that if work stops, you have some runway.

- Stay Flexible & Healthy: Update skills and network. The future workplace could change (AI, remote platforms). Stay in good health – exercise, eat well – so you can actually show up at 70+. Many 70-year-olds are fitter than some 50-year-olds. Your body is a key asset; treat it as such.

- Plan for Pivots: Think outside one job. Freelancing, teaching, consulting, or even entrepreneurship can be gentler as you age. Some people like partial retirements (Phased Retirement programs let you work part-year).

Interactive Self-Audit:

- Do you have a Plan A (ideal work path) and Plan B (if things go south) for your late career?

- List your non-negotiables: health coverage, income level, work environment. Can you find them in the jobs likely to be available at 70+?

- What skills or certifications could you acquire now that would let you earn remotely or part-time in future?

- How far from current savings to sustainable retirement? If there’s a big gap, will you close it by working longer, by cutting spending, or by something else?

Treat this like a business plan for your life: it’s better to overwrite a few to-dos now than to be caught off-guard at 68.

Quick Self-Audit Checklist:

- ❏ Lifespan Check: At 65, can I reasonably expect to reach 80+? (Statistically likely.) Is my plan built for that?

- ❏ Health & Skills: Could I perform my job in 10-20 years? What would need to change?

- ❏ Income Sources: If I stopped working tomorrow, how much of my expenses would Social Security and savings cover? Could I make up the rest by working part-time?

- ❏ Emergency Plan: If I got sick or laid off at 70, do I have a cushion? Are disability and health policies reviewed?

- ❏ Retirement Mindset: Am I emotionally prepared to work well past 65 if needed? If not, what concrete financial target would let me actually retire instead?

Common Pitfalls to Avoid When Facing a Lifetime of Work

- Mistake: Skipping Savings, “I’ll Just Work Forever.” Even if you love your job, don’t assume paychecks last forever. The Kiplinger Q&A is blunt: “thinking you’ll never retire can’t be an excuse to put off saving”. You lose growth on those contributions and have no fallback if work ends early.

- Mistake: Betting on Guaranteed Health or Job Security. Many things can derail work plans: layoffs, industry changes, caregiving duties, or illness. Build redundancy. Assume the unexpected.

- Mistake: Ignoring Inflation & Healthcare Costs. Older adults face especially high inflation (healthcare, assisted living, etc). Plan for annual cost hikes. And long-term care costs can skyrocket; consider whether and how to insure or save specifically for them.

- Mistake: Underestimating Burnout. Working longer isn’t just a number game; it’s a lifestyle. Mixing shorter hours or a different career (consulting vs. retail, for instance) can prevent fatigue. Soul-crushing work won’t be sustainable.

- Mistake: Financial Tunnel Vision. Work gives income, but don’t neglect taxes and benefits: high earnings at 70+ can increase Medicare premiums or tax on Social Security. Understand those trade-offs.

- Mistake: Going It Alone. No one navigates this without support. Use social networks and advice: financial advisors, retirement coaches, or simply peers in your situation. Plan together or at least talk it out.

Frequently Asked Questions

Q: Do I really have to work for the rest of my life?

Not necessarily. It’s not literally “life” unless you choose it. But realistically, many of us can’t afford to stop at 65. The key is planning. Some might find ways to retire around 70 by cutting expenses or using part-time work; others will work on because of passion or finances. Remember Kiplinger’s takeaway: “Only 28% of retirees hit their target date” – plans change. The goal is flexibility, not rigid “retire by X age.”

Q: Why do we have to work forever?

There’s no grand conspiracy; it comes down to money and longevity. We’re living decades longer with shaky support systems. Pensions are rare, Social Security was never meant to cover 30+ years, and costs (healthcare, housing) keep rising. Economists suggest one solution: work longer to delay tapping savings. Labor force stats back it: participation for ages 65+ is climbing towards 20%. So “having to” work is often about making the math work out.

Q: What if I hate my job or can’t physically do it at 80?

Then you have to adapt. Working longer doesn’t mean staying in the exact same role. Many seniors switch to lighter duties, part-time work, or new fields (teaching, consulting, crafts). The concept of phased retirement or encore careers is growing. If you absolutely cannot work, then planning earlier is crucial – either save more upfront or build an income stream (like investments, rental property) that isn’t tied to physical labor.

Q: Why would someone want to work forever?

Surprisingly, there are upsides:

- Financial cushion (tax advantages, growth on capital).

- Better Social Security and pension outcomes (8% per year boost).

- Mental and physical benefits (study after study shows post-retirement work keeps the mind sharper and body active).

- A sense of purpose and social connection (imagine ditching daily routine vs. enjoying it). Some people simply don’t see retirement as “fun.” Tom, our techie, enjoys mentoring colleagues; others find passion in a hobby turned job.

Weigh these against the downsides. If you’re choosing to work because it adds fulfillment and security, it can be a great path.

Q: How did real people come to terms with working forever?

In our interviews, we heard two main paths: Resignation and Reframing. Sandy McConnell (80) boiled it down: if her money is zero and bills exist, she has “no choice” but to keep working. Others, like our Tom, reframed it as a privilege – a chance to stay active. The advice: cultivate a positive outlook and make work fit your values. If you can’t quit mentally, schedule “mini-retirements” (sabbaticals, switching gears, or volunteering) throughout your later years to stay engaged.

Q: How can I boost my savings if I fear working forever?

Focus on tax-advantaged vehicles now (401(k), IRA, HSA). The younger you start, the more compounding helps – a 25-year-old extra $5k/year is huge. Later, continue maxing out and avoid early withdrawals. Reduce unnecessary spending (especially debt). Every extra dollar you save reduces the pressure to have to work. Also, consider home equity or annuities carefully as supplemental income if needed.

Q: Are there alternatives to “work forever”?

Sort of. You could aim for Financial Independence earlier (FIRE movement), which some do by extreme saving/investing. Or downsize drastically and live more frugally. Some choose to combine work with travel (digital nomads retiring on the road). But in all cases, you still rely on either some income or very low expenses. The reality is, unless you win the lottery, money or work will touch you until you die. The question is optimizing each.

Action-Oriented Conclusion & Next Steps

You’ve got a playbook now for confronting a “work forever” life. The truth is, most of our grandparents couldn’t have imagined this future, but here we are. If you end up working into old age – whether by plan or by surprise – you can still win. Plan early, be smart with money, stay healthy, and keep an open mind.

Remember: Working longer is not a curse if it’s done by choice and preparation. You can treat every extra year on the job as a “raise” on your retirement. Plus, you are not alone. As one expert reminds us, people are indeed living to 100, so planning for that is simply wise.

You have got this. Now breathe: one step at a time. Update your retirement spreadsheets, talk to a financial advisor, and start small adjustments like maxing out that 401(k) a bit more or learning a new skill for future income.

Next up: Now that your long-term plan is set, tighten up the details. For example, You earned a lot then brock. Check out our guide on [The Income Skills vs Money Skills Truth] to keep your current balance and future balance growing for the journey ahead.

What part of “working forever” worries you the most—money, health, boredom? Let’s discuss in the comments. And if this guide helped you rethink your plan, subscribe to TheFitFinance newsletter for more deep dives into securing your financial future at any age.